Western Digital’s February 2026 Innovation Day showed a company fundamentally transformed from its legacy PC-centric storage roots into a critical AI infrastructure provider. The presentations unveiled breakthrough innovations that challenge long-held assumptions about hard drive technology limits:

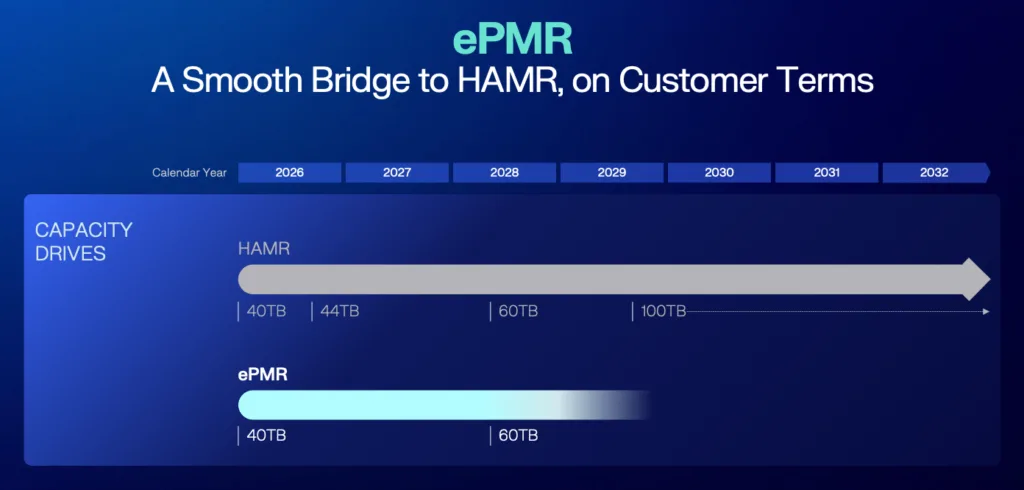

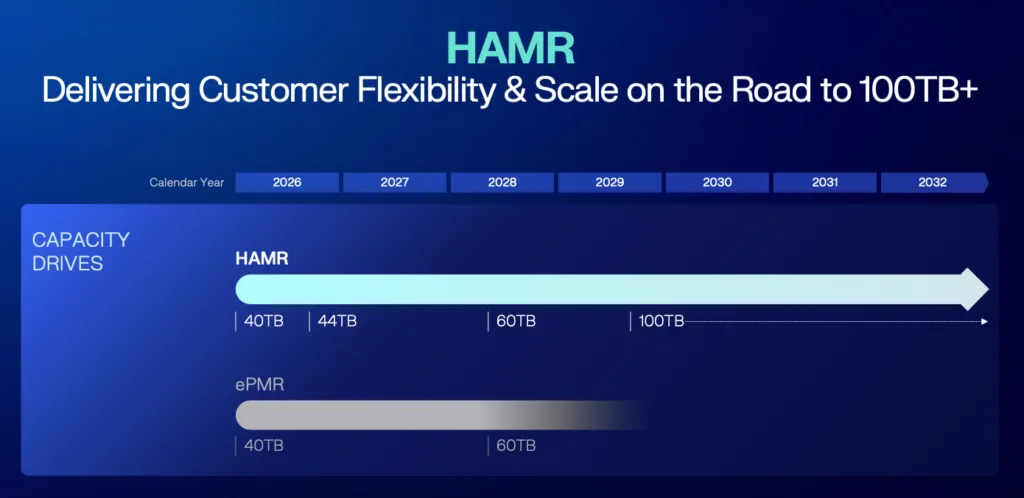

- Technology roadmap acceleration extends ePMR to 60TB (previously thought limited to ~36TB) while advancing HAMR to 100TB by 2029 through proprietary laser technology

- Performance innovations deliver 2-3x bandwidth improvements and 2x IOPS gains without customer infrastructure changes—challenging QLC flash economics in cloud storage tiers

- Financial model upgrade projects >20% revenue CAGR, >50% gross margins, >40% operating margins, and >30% FCF margins, targeting >$20 EPS within 3-5 years

- Pricing paradigm shift from historical mid-to-high single-digit annual declines to stable/positive pricing based on customer value delivery

- Market position strengthening with 90% revenue tied to data center/cloud/AI and long-term customer commitments extending through 2027-2028

At its recent “Innovation Day” in New York, Western Digital showed off a remarkable business model transformation following its mid-2025 flash business separation. The company now derives 90% of revenue from data center, cloud, and AI workloads, a dramatic shift from its historical consumer and PC-centric focus.

This has fundamentally altered WD’s business characteristics from seasonal/cyclical to secular growth aligned with long-term data center buildout trends.

The company also rebranded to “WD” with new visual identity emphasizing its data center positioning. CEO Tiang Yew Tan framed the company as being “at the heart of AI and cloud,” with hard drives serving as the “beating heart of AI” storage infrastructure.

Management highlighted organizational changes including deeper customer engagement structures, engineering talent recruited from hyperscalers who understand cloud architecture requirements firsthand and strengthened leadership across functions.

Its customer-obsessed approach has translated into multi-year purchase agreements with major hyperscalers extending through calendar 2027-2028, providing unprecedented demand visibility.

Let’s look at what the day revealed.

Technology Roadmap: Breaking Previous Limits

Chief Product Officer Ahmed Shihab presented the most comprehensive hard drive innovation roadmap the industry has seen in years, with technologies addressing capacity, performance, power efficiency, and ease of adoption.

ePMR Extension

WD shattered industry assumptions that ePMR technology peaks at about 36TB with announcements that demonstrate continued viability:

- 40TB ePMR drive currently in customer qualification (announced last week with first hyperscaler, second added today)

- Roadmap extending to 60TB ePMR through material science advances, head design optimization, and triple actuation technology

- 11-platter design scaling to 12 platters for higher capacities

- Same power envelope maintained throughout capacity scaling

WD’s extended ePMR roadmap serves dual strategic purposes: (1) provides proven, high-yield technology for customers requiring immediate capacity with minimal risk, and (2) creates smooth transition overlap with HAMR adoption, allowing customers to qualify both technologies and choose deployment timing based on their infrastructure readiness.

HAMR Acceleration and Roadmap to 100TB

WD’s HAMR program is progressing well:

- Volume ramp pulled forward 6 months to first half 2027 (from previous 2H27 guidance)

- Currently qualifying 40-44TB HAMR drives with two hyperscale customers

- Based on proven 11-platter ePMR platform for reliability and smooth transition

- Same firmware as ePMR drives to ensure infrastructure compatibility

- Already demonstrating 4TB per platter areal density in labs (44TB total capacity)

The HAMR roadmap extends to 100TB by 2029:

- Proprietary laser technology (6 years in development, now operational in labs):

- Vertical-cavity surface-emitting design vs. industry-standard edge-emitting lasers

- More efficient light utilization for higher areal density

- Shorter form factor enables closer platter spacing

- Independent head/laser testing improves manufacturing yields

- Enables 4TB to 10TB per platter areal density progression through 2028

- Increased platter count:

- New laser design allows packing 14 platters into standard 3.5″ form factor

- Combined with 10TB per platter = 140TB theoretical capacity

- Common platform approach:

- ePMR and HAMR share mechanical platform and manufacturing lines

- Reduces transition risk and capital requirements

- Enables fungible production capacity

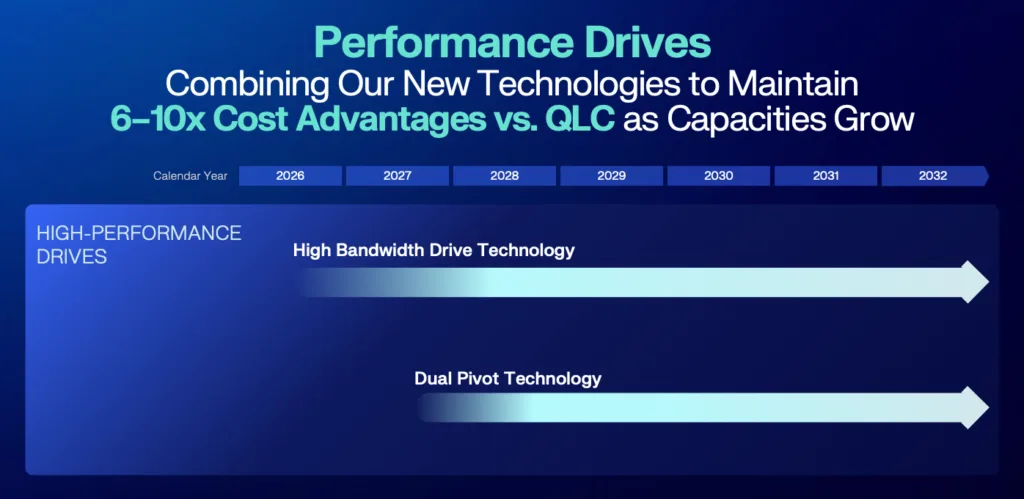

Performance Drives: Challenging Flash Economics

WD demonstrated two breakthrough performance technologies that fundamentally alter the hard drive value proposition for AI workloads.

High-Bandwidth Drives

Traditional HDDs deliver 200-250 MB/s sequential throughput. WD demonstrated drives achieving 500+ MB/s, fully saturating the SAS interface that connects drives to network infrastructure in hyperscale deployments.

Key points:

- Achieves performance parity with QLC SSDs in deployed configurations (not theoretical specs)

- QLC drives spec at 6 GB/s, but when deployed through standard SAS interfaces in object storage architectures, deliver <530 MB/s (the same bottleneck as HDDs)

- 10x lower cost than QLC for equivalent deployed performance

- No customer infrastructure changes required (same boxes, software, network)

- Technology is scalable to 4-8x current HDD performance as capacities increase to 100TB

- Introduction planned at 50TB capacity point

- Currently in customer hands for testing

Dual-Pivot Actuator Technology

WD demonstrated dual independent actuator arms that double IOPS to match increased bandwidth:

- Operates as single logical drive to host with no software changes required

- Fits in existing customer chassis without modifications

- Manufactured on same production lines as single-actuator drives

- No additional power consumption

- Introduction planned at 60TB capacity

- Customer testing begins late 2027-2028

This contrasts sharply with previous dual-actuator attempts (by WD and competitors) that required hardware changes, software modifications, and increased power.

Power Optimization: New Storage Tier

WD introduced a third variant targeting a new storage tier between primary and archive:

- 20% power reduction through optimized spin characteristics

- Only 5-10% sequential I/O performance penalty

- 10% capacity bonus (additional 10TB at 100TB drive sizes)

- Addresses inference-generated data that doesn’t require cool-tier performance

- Same infrastructure, software, and manufacturing compatibility

- Qualification begins 2027

Simplified Adoption: Platform for Neo-Clouds

Targeting emerging AI companies lack hyperscale engineering resources to optimize for UltraSMR and advanced HDD features, WD announced a platform approach with open APIs:

- Abstracts HDD complexity (UltraSMR, high-bandwidth, dual-pivot, capacity management)

- Available on both flash and HDD to ease migration paths

- WD handles qualification and optimization behind API

- Targets “Neo-cloud” segment building AI infrastructure

- Launches 2027

This directly addresses an untapped TAM where companies have chosen flash by default due to integration complexity rather than technical requirements.

Market Dynamics: AI-Driven Secular Growth

WD articulated three overlapping AI-related demand drivers:

- Training data storage: Multimodal LLMs (especially video-based models) requiring massive training datasets

- Inference-generated data: Every query/prompt generates context that must be stored persistently, creating exponential data growth

- Edge AI applications: Autonomous vehicles and robotics deploying multimodal models generating sensor and operational data

Combined impact: 25%+ nearline exabyte CAGR over next 5 years, with HDDs maintaining 80% share of hyperscale storage (with potential for expansion given performance improvements).

Pricing Transformation

Perhaps the most significant shift in WD’s business model is the pricing environment transformation.

Historical Model:

- Annual ASP per TB declines of mid-to-high single digits

- Pricing driven by competitive dynamics and technology cost curves

- Volatility based on supply/demand imbalances

New Model:

- Stable pricing environment: flat to low single-digit increases per TB

- Calendar 2026 projection: mid-to-high single-digit ASP per TB increases YoY across all four quarters

- Pricing tied to customer value delivery rather than cost curves

- Customers explicitly requesting pricing predictability for multi-year data center planning

Sennesael was emphatic: “For me, pricing is fully tied to how much value we deliver to our customers. It has nothing to do with tightness in the supply chain or strength in the cycle or weakness in the cycle.”

This is a departure from historical HDD economics and appears validated by multi-year customer agreements and performance-based value propositions.

Competitive Positioning

While competitor Seagate was not explicitly discussed, WD’s announcements have clear competitive implications.

Capacity Leadership:

- WD’s 40TB ePMR matches or exceeds publicly known competitor roadmaps

- 60TB ePMR extends lead if competitors cannot match aerial density improvements

- 100TB HAMR by 2029 appears ahead of known competitive timelines

- Proprietary laser technology (versus industry-standard edge-emitting) creates potential cost/density advantages

Platform Commonality:

- ePMR/HAMR sharing 11-platter mechanical platform reduces transition risk

- Competitors using 10-platter HAMR designs may face cost disadvantages at equivalent capacities

- Manufacturing fungibility provides supply chain flexibility

Performance Differentiation:

- High-bandwidth and dual-pivot technologies appear unique in HDD industry

- No direct competitor announcements matching 500 MB/s HDD performance or doubling IOPS without infrastructure changes

Customer Lock-In:

- Multi-year agreements with major hyperscalers create switching costs

- Deep engineering integration (pre-qualification testing during development) strengthens relationships

- Recording-technology-agnostic approach (smooth ePMR/HAMR overlap) reduces customer risk versus forced transitions

Analysis

Western Digital’s 2026 Innovation Day told a compelling transformation story backed by tangible financial results and credible technology demonstrations. The company has executed remarkably well over the past 12-18 months post-separation, and management’s confidence is clearly elevated.

What Works:

- The customer-centric pivot is genuine and strategically sound. Having executives with hyperscale experience (Ahmed Shihab from AWS/Microsoft) fundamentally changes product development from technology-first to requirements-first approaches.

- The technology roadmap directly addresses stated customer needs (capacity, performance, reliability, smooth transitions, power efficiency) rather than pursuing innovation for its own sake.

- The pricing environment transformation, if sustainable, may be the most significant change in HDD industry economics in recent memory. WD’s argument that pricing should reflect customer value rather than cost curves is sound, and the multi-year customer agreements suggest acceptance.

Western Digital’s 2026 Innovation Day revealed a company that has successfully transformed its business model, technology roadmap, and financial profile in remarkably short timeframe. The shift from PC-centric storage provider to AI infrastructure enabler positions WD at the center of one of technology’s highest-growth segments.

WD’s technology innovations are substantial and credible. If executed as planned, the capabilities will provide differentiated competitive positioning and support the aggressive financial model targets.

WD’s tech demonstrations were impressive and appeared genuine (not vaporware). The 40TB ePMR drive is shipping to customers today. HAMR drives are in qualification. High-bandwidth drives are in customer hands for testing. The dual-pivot technology was demonstrated on-site.

The proprietary laser technology is a potential game-changer if manufacturing execution matches lab results. Moving from 4TB to 10TB per platter by 2028 would provide significant competitive differentiation and cost advantages.

The performance innovations (high-bandwidth, dual-pivot) directly challenge the economic case for QLC flash in certain cloud storage tiers. WD’s argument about SAS interface bottlenecks limiting deployed QLC performance is technically sound and validated by customer testimonials (Microsoft’s Aaron Ogus).

If WD can deliver 2-3x HDD performance improvements at 10x lower cost than flash, it potentially alters storage tier economics.

Key things to monitor:

- HAMR reliability and adoption in large-scale customer deployments

- Areal density execution toward 10TB per platter targets

- Pricing discipline maintenance through demand cycles

- Customer qualification and deployment timelines for new technologies

- Competitive response from Seagate and potential flash alternatives

For technology buyers and IT infrastructure planners, WD’s roadmap provides confidence in hard drive viability for AI/cloud workloads through the end of the decade. The performance improvements and smooth transition pathways address key adoption concerns while maintaining cost advantages.

Western Digital is performing extremely well and is poised to continue as it meets the needs of data hungry AI infrastructure, especially in our current moment where QLC NAND flash will be supply constrained over the mid-term. This is WD’s moment, one the company recognizes and is seizing.