Last week, Marvell released its earnings for the second quarter of its fiscal 2024, demonstrating robust performance with $1.34 billion in top-line revenue. While that number was down year-over-year, it surpassed the midpoint of the company’s guidance.

Insight: Growth in Cloud & AI

Marvell’s data center business was a bright spot. Revenue from that business was $460 million, up 6% from the quarter prior. The growth in data center was primarily attributed to the increasing demand for Marvell’s optical products, which facilitate the expansion of cloud-based AI deployments.

Marvell experienced over 20% sequential revenue growth from cloud-related endeavors. Both Cloud AI and standard cloud infrastructure exhibited sequential revenue growth, with AI demonstrating accelerated expansion. Conversely, the enterprise on-prem segment experienced a significant sequential decline due to a weakening enterprise market.

Marvell’s technological advancements, particularly in optical connectivity, were crucial to its AI-focused growth. The company’s PAM4-based optical DSPs and AECs proved vital for connecting AI accelerator clusters within data centers, while its DCI products facilitated connectivity between regional data centers.

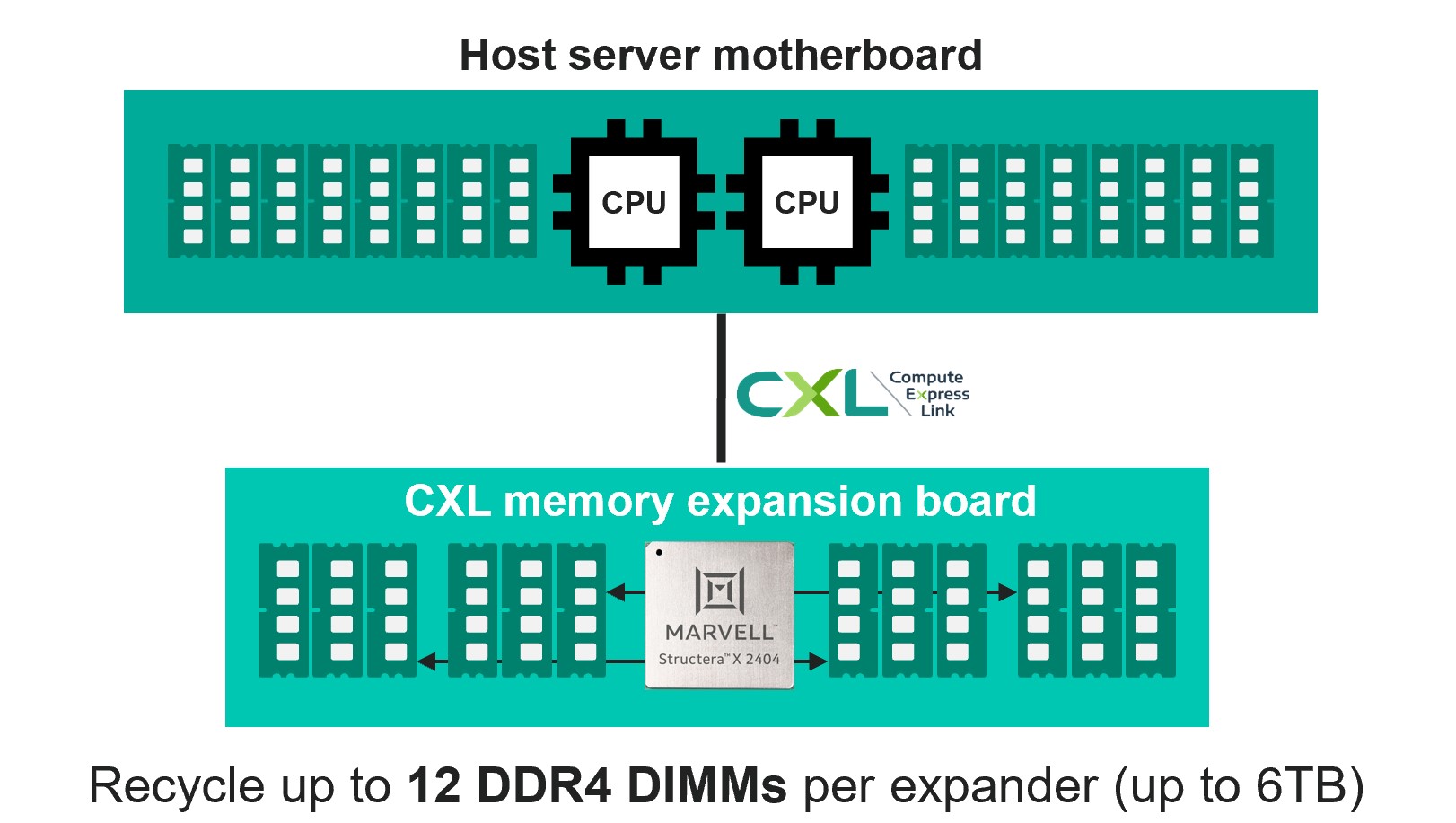

Marvell’s comprehensive range of solutions, which includes high-capacity Ethernet switches and custom silicon for compute acceleration, has the company positioned to capitalize on the burgeoning AI market. The success of Marvell’s 800-gig PAM4 DSPs and the announcement of its next-generation 1.6T platform indicated the company’s prowess in high-speed connectivity solutions. Furthermore, Marvell’s commitment to advancing its Orion coherent DSP and Ethernet switches underscored its leadership in optical technology.

Automotive Strength

Marvell’s revenue exceeded expectations in the automotive and industrial segments, showing a notable 32% year-over-year growth. The adoption of Ethernet in vehicles contributed to this success, along with new design wins with major automotive OEMs. Marvell projected continued year-over-year growth in this segment, emphasizing the increasing prevalence of Ethernet in the automotive industry.

The automotive segment will continue to be a high-growth segment for Marvell as the automotive industry continues its shift away from legacy in-vehicle interconnects toward an ethernet-based zonal architecture. According to Marvell, the number of automotive ethernet ports shipped annually is growing at nearly 40% year-over-year, with shipments expected to surpass one billion ports annually by 2025. That’s a lot of switches.

Marvell’s approach to automotive is paying off. The company collaborates with over 40 automotive OEMs and has design wins with eight of the largest automakers.

The momentum should continue for Marvell. Earlier this summer, the company introduced its latest generation automotive networking products with its new Brightlane Q622x family of automotive ethernet switches. The new product is the highest capacity switch in the segment, delivering 90 Gbps of bandwidth, double the capacity of currently available automotive switches.

Analysis

While Marvell is showing good growth in cloud, AI, and automotive, the news is less good for its storage and non-cloud data center business. Company CEO Matt Murphy said on the earnings call that the storage end market “remains significantly depressed and customer inventory remains high” and that recovery in that segment has been “pushed out meaningfully.”

This isn’t a Marvell-specific problem; it’s consistent with what we’re hearing from other players in the storage market. Enterprise storage vendors Hewlett Packard Enterprise, Dell Technologies, and Pure Storage are all set to release earnings later this week, so we should know how the broader enterprise storage segment is performing.

Despite the challenges in storage and data center, Marvell is projecting accelerated growth from the cloud during 2H 2023. The continued expansion of cloud AI and standard cloud infrastructure will drive this growth.

Marvell is competitively strong, with one of the strongest portfolios across the segments it’s playing in. The company’s focus on AI applications, cloud growth, optical technology leadership, and strategic product introductions have Marvell well-positioned for continued success. Marvell’s outlook remains positive, with expectations of revenue growth acceleration and gross margin expansion in the third quarter. The company’s emphasis on advanced silicon for data infrastructure and its diversified end-market approach underscores its ability to thrive in dynamic market conditions.