Palo Alto Networks released its FQ3 2024 earnings, beating consensus on revenue and earnings, but disappointing with weaker than expected guidance. Let’s take a quick look at the company’s earnings.

Key Points from Q3 Earnings Call:

- Economic and Industry Context:

- The cybersecurity landscape is marked by escalating cyberattacks, including sophisticated nation-state activities targeting software supply chains and critical infrastructure.

- Organizations face the challenge of rapidly detecting and mitigating breaches, with detection times still lagging considerably behind the speed of attacks.

- Strategic Developments:

- Palo Alto Networks is heavily investing in AI to pace up with both the opportunities and threats brought by the technology. The company has launched a suite of AI security products designed to safeguard AI applications in organizational settings.

- The company’s platformization strategy is proving effective, with significant uptake in customer engagement and an increase in sales centered on this approach.

- Financial Performance:

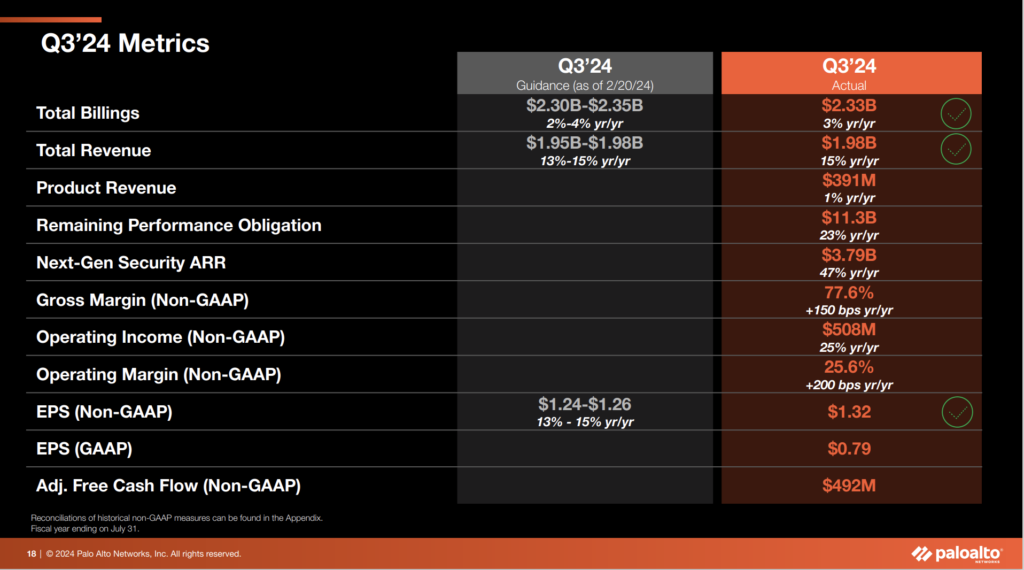

- The company reported a strong Q3 with a 15% growth in revenue and improvements in operating margins by 200 basis points year-over-year.

- Despite a preference among customers for annual billing which impacts the billing metrics, the company’s deferred bookings and backlog show positive trends.

- Innovation and Product Launches:

- Ongoing innovations include the launch of next-generation security capabilities and enhancements in their SASE product lineup.

- Notable product launches include AI-powered data security tools integrated into SASE, application acceleration features, and enhancements in cloud security platforms.

- Market and Customer Dynamics:

- The company has seen a substantial increase in its platform sales, particularly those fully utilizing Palo Alto Networks’ capabilities across multiple security platforms.

- Strategic partnerships, like the one with IBM, are set to amplify the reach and integration of Palo Alto’s offerings, potentially leading to increased market penetration and customer base expansion.

- Future Outlook:

- Nikesh Arora is optimistic about the future, expecting the company to reach a next-generation security ARR of $15 billion by fiscal year 2030.

- The company anticipates continued strong demand and is positioning itself to capitalize on both current and emerging market opportunities, especially those related to AI and cloud transformations.

Analysis

Under the leadership of Nikesh Arora, Palo Alto Networks is navigating a complex cybersecurity landscape with innovative strategies and setting a strong financial trajectory.

The company’s focus on AI and platformization should keep it at the forefront of the cybersecurity industry, providing substantial growth and value creation potential, though its being increasingly challenged by strong and aggressive competitors with strong portfolios, including companies like SentinelOne and CrowdStrike. As Palo Alto Networks expands the breadth of offerings, this will only increase.

As Palo Alto Networks moves forward, it remains well-positioned to meet the evolving needs of its global customer base, reinforcing its market leadership in cybersecurity solutions.