Hard Disk Drive manufacturer Quantum announced its FQ1 2025 earnings, beating Wall Street estimates on earnings and missing slightly on revenue. The earnings reflect both the challenges and opportunities the company faces as it continues its strategic transformation.

Let’s look at what the company reported.

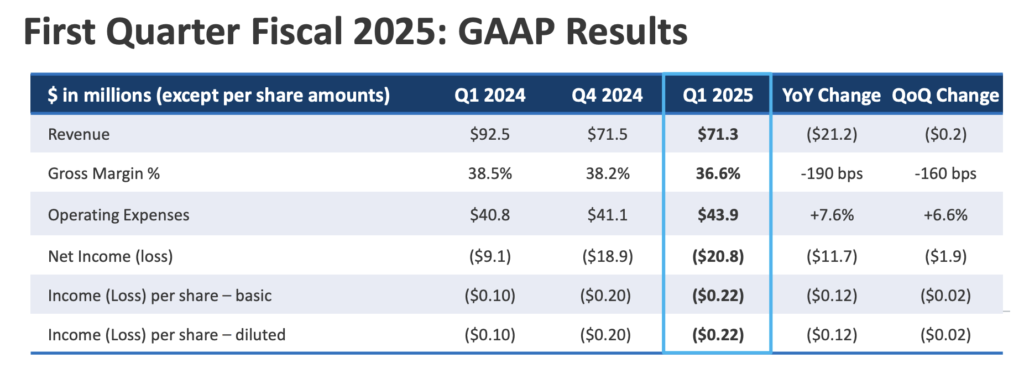

Financial Highlights

- Revenue: $71.3 million, a 23% decrease year-over-year.

- Non-GAAP Gross Margin: 36.9%, slightly down from the prior quarter’s 38.5%.

- Adjusted EBITDA: Negative $3.1 million, compared to a positive $1.5 million in Q1 FY24.

- GAAP Net Loss: $20.8 million, or a loss of $0.22 per share.

- Supply Chain Impact: Continued constraints leading to higher manufacturing costs and increased backlog of $15.5 million.

Strategic Progress

Quantum is undergoing significant transformation, focusing on long-term growth initiatives and restructuring its operations to enhance profitability and efficiency.

The company made substantial progress in the following areas:

- Increased Liquidity:

- Secured over $25 million in new growth capital.

- Restructured $110 million in existing debt, improving the overall capital structure and balance sheet.

- Focus on Key Platforms:

- Myriad Platform: Gaining traction, particularly in AI-driven unstructured data management.

- ActiveScale Platform: Saw several notable wins, including a significant deal with an NBA team for more than 10 petabytes of active and cold storage.

- Product Development:

- Successful launch of the DXi T10 product in the enterprise backup market, with multiple deals closed shortly after the announcement.

- Continued investment in engineering and product development, especially in subscription-based solutions.

Financial Metrics & Performance

- Revenue Decline: The year-over-year revenue decrease was primarily due to the loss of a major hyperscaler customer and ongoing supply chain issues.

- Gross Margin: The gross margin dipped slightly due to a large-scale strategic video surveillance sale and supply constraints affecting high-margin product shipments.

- Cost Controls: Non-GAAP operating expenses decreased to $30.8 million from $35.5 million, reflecting proactive efforts to improve operational efficiency.

- Annual Recurring Revenue (ARR): $141 million, with a 29% year-over-year increase in subscription ARR.

Guidance & Outlook

Quantum provided guidance for the second quarter of fiscal 2025:

- Revenue Expectation: Approximately $73 million, plus or minus $2 million.

- Non-GAAP Operating Expenses: Expected to be around $30 million, reflecting continued cost control measures.

- Adjusted EBITDA: Projected to be breakeven, driven by anticipated improvements in gross margin and continued operational efficiency.

Quick Take

Quantums’s FQ1 2025 earnings show a company amid a challenging yet promising transformation. While the immediate financial results may raise concerns, its strategic initiatives and operational improvements underway provide a foundation for future growth.

For the first quarter of fiscal year 2025, Quantum reported revenues of $71.3 million, a steep 22.9% drop compared to the same period last year. This shortfall was compounded by the loss of a major hyperscaler customer, underscoring the risks associated with heavy dependence on a few large clients. The company also faced accounting issues that necessitated the restatement of financial results for previous years, further complicating its financial reporting.

Quantum is also moving towards a subscription-based sales model, a strategy that many in the storage industry are adopting. This shift is beginning to pay off, with the company’s subscription annual recurring revenue (ARR) rising 29% year-over-year to $18.8 million.

Looking ahead, Quantum’s ability to navigate the decline of its traditional tape business while capitalizing on emerging opportunities in object storage and AI-driven data solutions will be critical. The company’s leadership is focused on improving operational efficiency and driving new product adoption, as it works to reverse the recent revenue declines and return to profitability.

While challenges remain, Quantum’s strategic shifts and ongoing efforts to innovate in high-growth areas offer a glimpse of hope for a company that has faced significant headwinds. The road ahead will require careful execution, but with the right moves, Quantum aims to carve out a stronger position in the evolving data storage landscape.