Rubrik reported impressive financial results for its Q2 FY2025, significantly outperforming key metrics and analyst expectations while raising its full-year guidance. The company attributes its strong performance to its leadership in the growing cyber resilience market, supported by its AI-powered platform, Rubrik Security Cloud, which integrates Data Security Posture Management (DSPM) with cyber recovery.

Financial Highlights

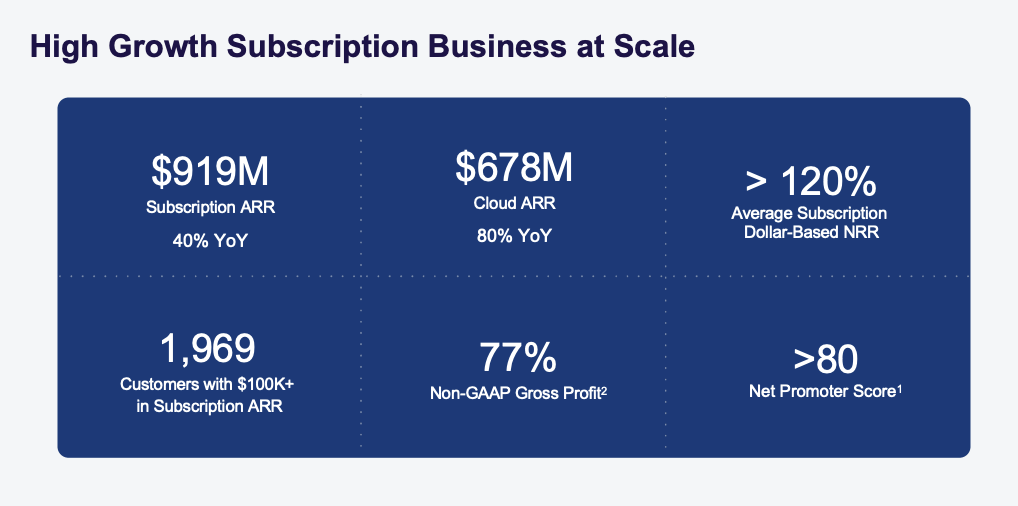

- Subscription ARR: $919 million, up 40% YoY.

- Subscription Revenue: $191 million, up 50% YoY.

- Net Revenue Retention (NRR): Over 120%.

- Subscription ARR Contribution Margin: Improved by over 1,300 basis points YoY.

- Total Revenue: $205 million, up 35% YoY.

Key Drivers

- Leadership in Cyber Resilience: Rubrik’s platform gives the company a solid position within the cyber resilience space.

- Differentiated Product Offering: Rubrik’s Security Cloud platform, which combines DSPM and cyber recovery under a Zero Trust architecture, is a key differentiator for the company. Its AI-driven architecture enables faster, more efficient cyber recovery than competitors, with Rubrick claiming recovery times of about 35 seconds compared to hours with other solutions. Rubrik says that this has led to it securing significant deals in the finance, insurance, and healthcare sectors.

- AI and Machine Learning Capabilities: Rubrik’s platform leverages AI for data risk analysis, data threat detection, and rapid recovery. Integrating DSPM with cyber recovery provides a comprehensive view of data security risks before, during, and after attacks, making Rubrik’s solution highly attractive to enterprises with complex cloud and on-premises workloads.

- Partnerships and Ecosystem Expansion: Rubrik’s new partnerships, particularly with Mandiant (a part of Google Cloud), strengthen its market position. The collaboration offers an end-to-end solution combining cyber threat detection, incident response, and data recovery. Additionally, Rubrik was recognized as Microsoft’s Healthcare and Life Sciences Partner of the Year for 2024.

Operational and Profitability Improvements

Rubrik has shown considerable progress in improving business efficiency and profitability, beating Wall Street EPS estimates by about 18%. The company’s subscription ARR contribution margin improved by over 1,300 basis points YoY, driven by cost efficiencies, growing sales force productivity, and enhanced operational leverage. Sales and marketing expenses as a percentage of revenue decreased by 1,200 basis points, highlighting Rubrik’s successful focus on profitability.

Outlook & Guidance

Given Rubrik’s strong performance and leadership in a growing market, the company raised its full-year guidance:

- Subscription ARR is expected to reach $1.026 billion to $1.032 billion, implying 31%-32% YoY growth.

- Total Revenue is expected in the range of $830 million to $838 million, up 32%-33%.

- Non-GAAP Subscription ARR Contribution Margins are forecasted between -7% and -6%, showing continued improvement.

Quick Take

Rubrik’s Q2 earnings showcase its growing footprint in the cyber resilience market, supported by its innovative AI-driven platform and expanding partnerships. The company’s ability to enable its customers to rapidly recover from cyberattacks, combined with improvements in business efficiency and profitability, keeps it well-positioned for continued growth.

With increasing demand for cyber resilience solutions and favorable macro trends, Rubrik is expected to continue outperforming in future quarters. We remain bullish on the company’s long-term growth trajectory and ability to capture and grow significant market share.