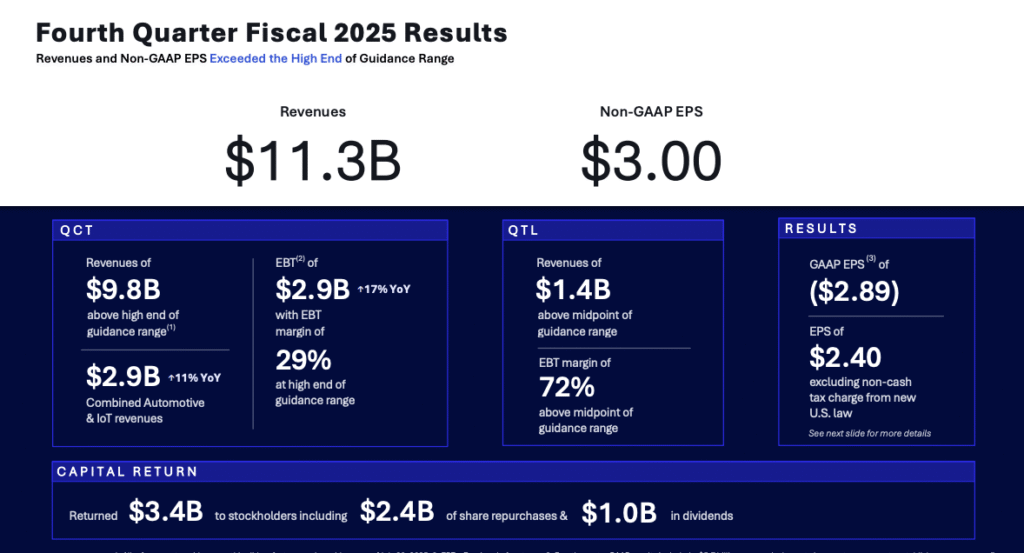

Qualcomm’s fiscal Q4 2025 results tell a story that extends far beyond the smartphone chips that built the company. While the guidance-busting earnings numbers, $11.3 billion in revenue and $3.00 EPS, are impressive, it’s not the full story.

The real narrative lies in three strategic vectors that collectively represent Qualcomm’s most ambitious expansion since the original Snapdragon launch: automotive systems, edge AI platforms, and data center inference accelerators.

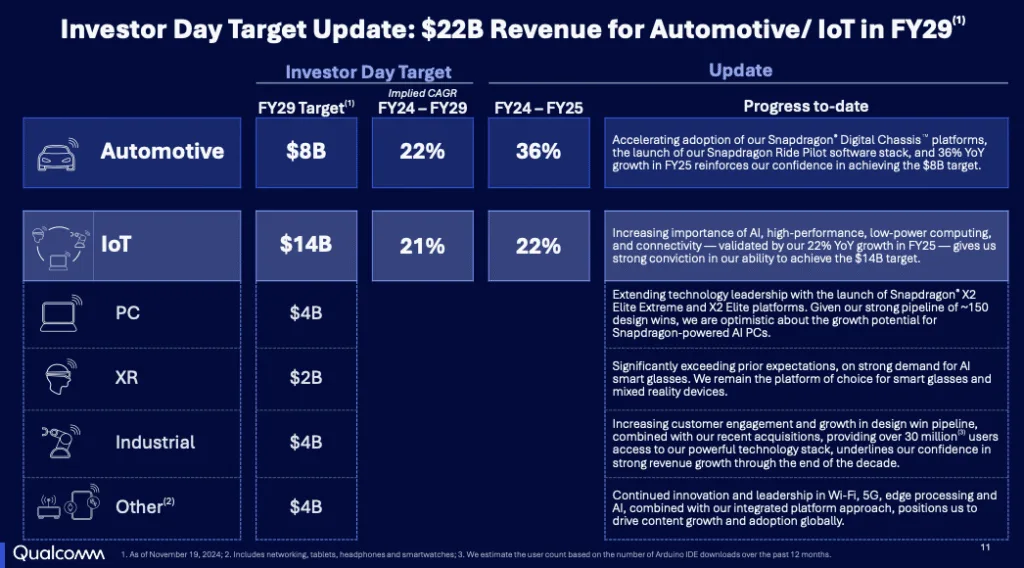

While data center is a new segment for Qualcomm, the company did lay its long-term revenue targets at its most recent investor day:

Automotive Crosses the Billion-Dollar Threshold

Qualcomm’s automotive segment achieved a symbolic milestone in Q4, surpassing $1 billion in quarterly revenue for the first time, growing 17% year-over-year. The number isn’t a surprise if you’ve been watching Qualcomm’s execution in this market:

- Validated across 60 countries, expanding to 100 by 2026

- 30 new ADAS design wins secured in Q2 FY2025 alone

- Design-win pipeline valued at $45 billion in future orders

- On track for $8 billion annual automotive revenue by fiscal 2029

There are some significant highlights from the past quarter worth calling out:

- BMW Engagement: The Snapdragon Ride Pilot system, now shipping in the BMW iX3 electric vehicle, delivers Level 2+ driver assistance through an integrated stack combining perception, planning, and control.

- Google Gemini Integration into Snapdragon Digital Chassis: This enables automakers to deploy multimodal AI assistants that function in both cloud-connected and offline modes—addressing latency, privacy, and connectivity constraints simultaneously.

The Google relationship also positions Qualcomm’s silicon as the bridge between on-device intelligence and cloud-scale models, transforming vehicles from data collectors into inference platforms.

Edge AI and IoT: Owning the Developer Ecosystem

Qualcomm has been steadily growing its IoT and intelligent edge business. IoT revenue reached $1.8 billion in Q4, up 7% year-over-year, driven by:

- Industrial and networking segments

- Wi-Fi 7 access points

- Fixed-wireless customer premises equipment

- On pace for $14 billion annual revenue by fiscal 2029

Building an Ecosystem

During the past quarter, the company acquired IoT company Arduino. The acquisition is part of a deliberate strategy to own the embedded AI developer experience from silicon to software stack.

Arduino brings 30 million developers. Combined with earlier acquisitions, this gives Qualcomm a vertically integrated toolchain:

- Edge Impulse: Edge ML development platform

- Foundries.io: IoT device management

- Arduino: Hardware ecosystem and developer community

The newly launched Arduino UNO Q, powered by Qualcomm’s Dragonwing processor, extends this into smart home automation, industrial robotics, and small-form-factor autonomous systems.

The success of these acquisitions is critical for Qualcomm. Selling into the IoT market, which is a high-volume/low-ASP play across a broad range of customers, is very different from Qualcomm’s traditional businesses.

If there’s one thing I’m most watching, it’s how Qualcomm builds both its channel and its brand equity in this space. It’s making the right moves, but it’s still early days.

Data Center Inference: A Big Bet Against GPU Hegemony

Qualcomm’s entry into AI data center compute represents its boldest strategic gamble, and potentially its most disruptive.

The company recently announced its upcoming AI200 and AI250 rack-scale inference accelerators.

During the earnings call, CEO Cristiano Amon framed Qualcomm’s competitive differentiation around two architectural advantages:

- Power-efficient Oryon CPU for head nodes and general-purpose compute inside AI clusters

- Novel inference architecture that departs from GPU + HBM conventions in favor of simplified memory hierarchies and SoC-level integration to maximize “tokens per watt”

The design philosophy of using DDR/LPDDR memory with tight CPU-NPU coupling is a fundamentally different approach than NVIDIA’s GPU-centric model or AMD’s Instinct accelerators. So is its use of PCIe as the scale-out fabric for these accelerators.

Qualcomm is betting that hyperscalers operating at megawatt scale will prioritize throughput per watt and total cost of ownership over raw performance.

It’s too early to know if Qualcomm’s bet is the right one (the first parts are still a few quarters away), but there’s chatter among analysts that Qualcomm’s approach may not deliver the performance needed. It’s a fair caution, but one that we really can’t answer until we have more technical details on the new solutions.

I’ll give them the benefit of the doubt on this one until we know differently, especially given the company’s early traction:

- First large customer: HUMAIN, targeting 200-megawatt deployment in 2026

- Moved data center revenue outlook forward by a full year to fiscal 2027

- Expects multi-billion-dollar opportunity by FY29

- Detailed benchmarks and architectural specifications coming in 1H 2026

Oryon: Qualcomm’s Unifying Architecture

Underpinning all three expansion vectors is Qualcomm’s Oryon CPU, the company’s custom ARM-based core now spanning:

- Smartphones: Snapdragon 8 Elite Gen 5 (5 GHz, mobile-class efficiency)

- Laptops: Snapdragon X2 Elite (150+ designs expected through 2026)

- Automotive: Digital Chassis controllers

- Data centers: Inference accelerators

The integrated NPU offers multi-trillion-operations-per-second AI acceleration across all device classes, enabling consistent software environments and developer tools from wearables to rack servers.

This architectural consistency contrasts sharply with competitors that maintain separate CPU designs for mobile, PC, and data center markets. This makes it easier for OEMs to deliver end-solutions, while giving Qualcomm a tremendous amount of internal leverage as it expands into its new markets.

Financial Performance

Qualcomm’s diversification strategy is delivering measurable results:

FY2025 Results:

- Revenue: $44 billion (+13% YoY)

- EPS: $12.03 (+18% YoY)

- Free cash flow: $12.8 billion (nearly all returned to shareholders)

- QCT segment EBT margin: 29%

FY2026 Q1 Guidance:

- Revenue: $11.8–$12.6 billion

- EPS: $3.30–$3.50

- QCT EBT margin: 30–32%

By extending its silicon and software IP into automotive, edge, and data center markets, Qualcomm is building defensible positions in segments where it can leverage power efficiency and AI integration advantages:

- Automotive: Qualcomm challenges NVIDIA’s Drive platform and Intel’s Mobileye by offering a comprehensive digital chassis spanning infotainment, ADAS, and vehicle connectivity.

- Edge AI: the Arduino acquisition and ecosystem investments create developer lock-in that software platforms alone cannot replicate, potentially positioning Qualcomm as the embedded equivalent of what NVIDIA achieved in data center AI.

- Data Center: success is less certain but potentially most consequential. If Qualcomm’s power-efficient architecture proves viable for large-scale deployments, it could capture meaningful share of the multi-hundred-billion-dollar inference market without competing in the more crowded training segment.

What to Watch in 2026

The next twelve months will reveal whether Qualcomm’s architectural bets validate at scale:

1. Data Center Details (1H 2026): When Qualcomm releases performance metrics and architectural details, the industry will assess whether tokens-per-watt leadership translates to meaningful TCO advantages for hyperscalers.

2. Automotive Production: The BMW iX3 deployment and expansion to 100 countries will test whether Qualcomm’s digital chassis can achieve the reliability and regulatory compliance required for safety-critical systems. Nvidia also seems to have renewed vigor in this space, so we’ll be equally watching how the competitive dynamics might shift.

3. AI PC Market Share: With 150+ Snapdragon X2 Elite laptop designs expected through 2026, can Qualcomm take meaningful share from Intel and AMD despite x86 software compatibility advantages? I don’t track client, but it’s an important one to watch.

4. Edge AI Developer Adoption: The success of Dragonwing, and the broader embedded AI toolchain, will determine whether Qualcomm can own the next generation of intelligent edge devices the way it dominated smartphones.

Overall, Qualcomm’s FQ4 results show that the company’s multi-year diversification plan is both clear and yielding impressive results. It’s a sound strategy that, at this point, simply comes down to execution.