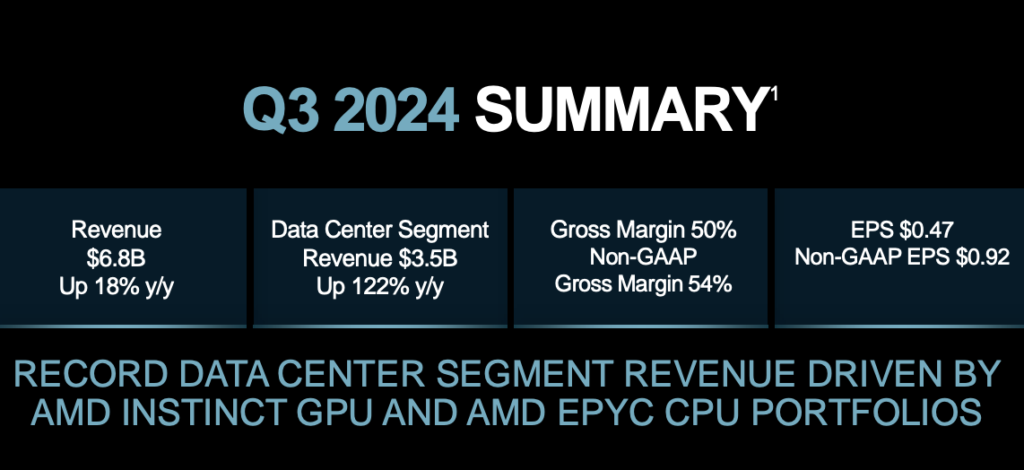

AMD this week announced significant revenue and earnings growth in Q3 2024, driven primarily by exceptional performance in the Data Center segment. AMD’s Data Center revenue increased by 122% year-over-year, reaching a record $3.5 billion and marking over half of AMD’s total revenue this quarter. CEO Lisa Su, on the earnings call, attributed this growth to the success of the EPYC CPUs and MI300X GPUs, which experienced strong adoption across cloud, enterprise, and AI applications.

Key Performance Highlights

- Revenue Growth: Total revenue for AMD reached $6.8 billion, a record high and an 18% increase year-over-year, fueled by record Instinct and EPYC product sales.

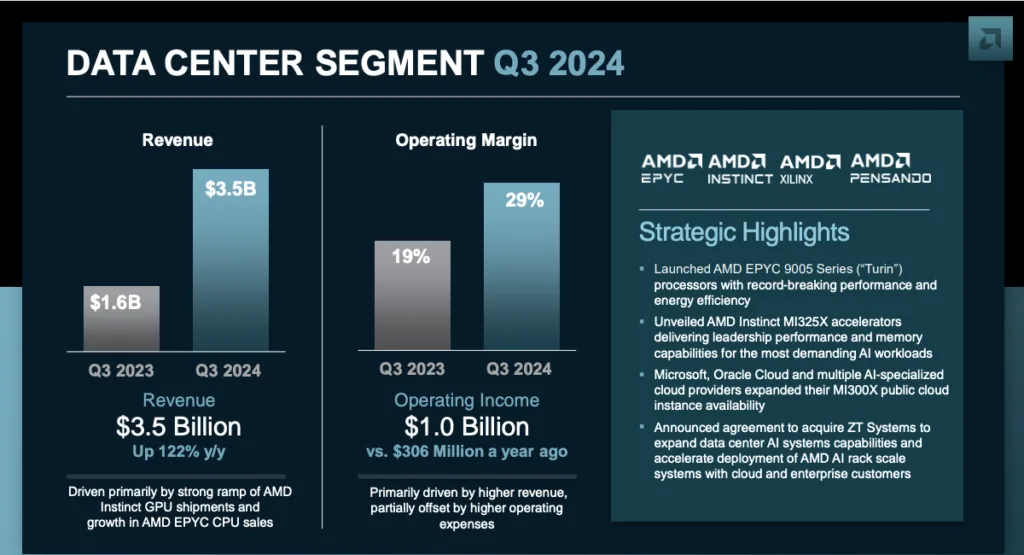

- Data Center Dominance: Data Center revenues of $3.5 billion represented a year-over-year increase of 122%, driven by AMD’s EPYC CPUs and MI300X GPUs’ broad adoption across major cloud providers, including Meta and Microsoft.

- Gross Margin and Earnings: Gross margin expanded by 2.5 percentage points, with a 31% increase in EPS, showcasing profitability improvements due to higher data center revenue.

Data Center Segment Analysis

- EPYC Processor Success: AMD’s EPYC CPUs have become a standard in modern data centers, providing superior total cost of ownership (TCO) benefits across enterprise and cloud workloads. AMD’s fifth-generation EPYC processors, now ramping up, offer leading performance that has driven adoption by major enterprises like Boeing, Adobe, and Boeing.

- MI300X GPUs and AI Applications: The MI300X GPU experienced substantial adoption within AI and inferencing applications, especially by major cloud providers like Meta and Microsoft, which use these GPUs to power models for large-scale AI applications. Public cloud offerings featuring MI300X instances increased, signaling AMD’s competitive positioning in AI infrastructure.

- Cloud Adoption and Enterprise Expansion: AMD’s data center products gained traction in both cloud and enterprise sectors, as demonstrated by expanded deployment by customers including Dell, HPE, Microsoft, and AWS. EPYC CPUs were integrated into cloud services for Office 365, Facebook, and Salesforce, while enterprise usage saw a sharp rise with major players like Siemens and FedEx adopting AMD solutions.

- Forward-Looking Product Developments: AMD launched the next-gen Turin processors in Q3, promising significant efficiency and performance advantages. AMD also advanced its AI accelerator roadmap with the MI325X GPU, enhancing its data center lineup and aiming for increased market share in AI infrastructure.

Strategic Acquisitions and Industry Alliances

- ZT Systems Acquisition: AMD announced its acquisition of ZT Systems, which will support AMD’s silicon and systems-level capabilities, enabling faster deployment of AI infrastructure. AMD plans to divest ZT’s data center infrastructure manufacturing segment post-acquisition, focusing on core systems expertise to accelerate AI development.

- x86 Ecosystem Alliance: AMD has formed an advisory group with Intel and industry partners to enhance compatibility and standardize innovations across the x86 platform, potentially strengthening its ecosystem and aligning it for future growth.

Outlook & Guidance

- Q4 2024 Forecast: AMD said that it expected Q4 revenue of approximately $7.5 billion, driven by continued momentum in the Data Center segment. Gross margin is expected to remain at 54%, with sequential growth projected across the Data Center, Client, and Gaming segments.

- Long-term Growth in AI Infrastructure: The Data Center Group expects revenues exceeding $5 billion in 2024, a substantial increase from initial estimates, reflecting the rapid adoption of AI technologies.

Analysis

AMD’s Data Center business continues to display remarkable strength, yielding a remarkable 122% year-over-year revenue surge to $3.5 billion in Q3 2024, which now represents over half of AMD’s total revenue. This segment’s growth is propelled by the strength of its EPYC CPUs and MI300X GPUs, with EPYC in particular gaining favor across cloud providers, enterprises, and hyperscalers due to its industry-leading performance and TCO advantages. AMD’s multi-generational EPYC lineup has enabled strong momentum, with major clients like Meta, Microsoft, and Boeing adopting EPYC processors for core applications and AI workloads.

At the same time, the success of the MI300X accelerators positions AMD as a top player in the AI data center space, especially in inference and training-heavy environments. While NVIDIA continues to dominate the AI GPU landscape, AMD’s expanding MI300X and upcoming MI325X GPUs are closing the gap by targeting specific performance metrics and energy efficiencies attractive to both hyper-scalers and enterprises.

AMD didn’t break out the revenue from processors and GPUs, but it was clear that the MI300 accelerator was a key contributor during the quarter. AMD’s EPYC processors also continue to see strength in the public cloud, where we know that the company is over-represented in AI configurations across nearly every CSP. We continue to watch the broader on-prem server business for signs of recovery, with OEMs like Dell and HPE set to announce earnings over the coming weeks. The reality for AMD is that it continues to execute and grow and is well-positioned to compete in enterprise inference- and fine-tuning-driven AI workloads.